Most of us don’t work for the fun of it. We work because our jobs give us money, and we can exchange that money for goods and services.

But are you getting the best bang for your buck, or are you spending money on stupid junk that doesn’t serve you?

Only you can decide – but perhaps comparing your budget to the best things to spend money on can help.

The Best Things To Spend Money On

We all want to spend our hard-earned cash on fun stuff, but that’s not always the answer.

The best things to spend money on are the things we need (because we have to survive, right?) and the things that make our lives worthwhile.

But our definitions of “things that make our lives worthwhile” probably aren’t the same.

What Do People Spend Their Money On?

Before diving into how you should spend your money, let’s take a look at what average consumers are doing.

Every year, the Bureau of Labor Statistics (BLS) publishes a report on consumer spending, showcasing how Americans spend their money.

The report is typically released in the fall and covers the previous year’s spending.

The most recent data, published in December 2025, shows consumer spending for 2024.

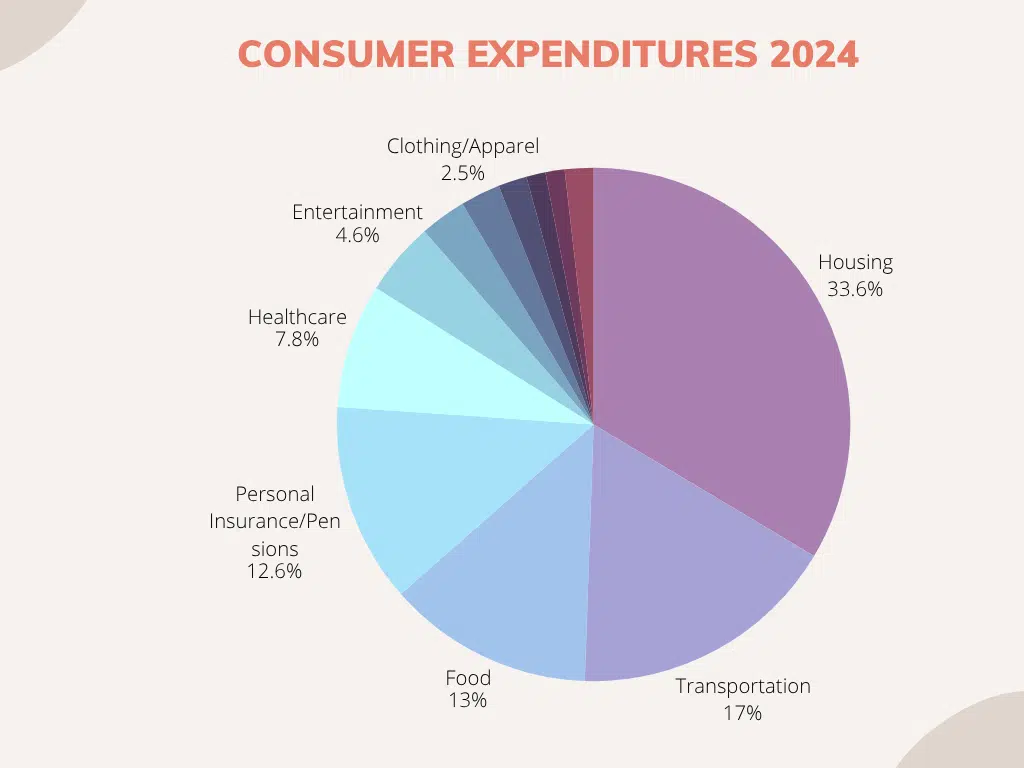

Here’s a pie chart showing the percentage of income Americans allotted to eight major spending categories in 2024:

How Americans Spend Money:

- 33.4% – Housing

- 17% – Transportation

- 12.9% – Food

- 12.5% – Personal Insurance/Pensions

- 7.9% – Healthcare

- 4.6% – Entertainment

- 2.9% – Cash Contributions

- 2.5% – Clothing/Apparel

- 2.0% – Education

- 1.2% – Vices (alcohol & Cigarettes)

- 1.2% – Personal Care

- 1.8% – Miscellaneous

People spend the bulk of their money on housing, transportation, food, insurance, and healthcare. That makes a lot of sense, because life is so expensive nowadays, and we need these things to survive.

What Should We Spend Money On?

People need a place to live, a way to get to work, food to eat, clothes to wear, and insurance to protect themselves from catastrophe.

But are we spending too much money on specific line items? Is there anything missing from the list?

Where Are Savings and Investments?

Personal savings and investments don’t appear on the list.

The personal insurance/pensions category includes social security, but doesn’t include other retirement savings.

The cash expenditures column captures things like child support, donations, gifts, and giving money to people outside the household (college students, friends, etc.).

None of the categories captures savings/investment.

What’s Left for Saving and Investing?

Savings technically aren’t “spending,” so it makes sense that they’re absent from a consumer expenditures report.

The Bureau of Economic Analysis (BEA) claims the average savings rate hovers between 3% and 4%.

That means on average, people are saving about $3,600 a year.

While it’s better than nothing, it’s not enough.

Averages Don’t Tell the Full Story

The situation gets even more dire when you realize how much “averages” skew the numbers.

The BEA data may be misleading because people with extremely high incomes may be stacking the savings rate, making it appear higher than it is by saving 30% of their income.

Kiplinger put out a great report comparing average retirement savings with median retirement savings, highlighting the vast disparity between the two numbers.

That, and the fact that over ⅓ of all Americans can’t cover a $400 emergency with cash, tells us that we’re not saving enough money.

Why Are Personal Savings Important?

Personal savings are crucial to a happy life.

Emergencies can happen at any time: cars break down, pets get sick, and hailstorms break windows. Having money set aside for these random occurrences is a lifesaver, allowing you to handle them right away with little stress.

Savings are also essential because we don’t want to work forever, and saving money means you won’t have to.

The bottom line is that people are spending too much and not saving enough.

What Do People Spend Too Much Money On?

The statistics show that people spend far too much on housing and cars.

Experts say we shouldn’t spend more than 30% of our income on housing.

These experts clearly haven’t noticed that housing prices have skyrocketed nationwide in recent years.

It’s harder and harder to find housing that only costs 30% of our income, so the national average of 33.4% isn’t that bad.

Of course, if you can cut back, you should, but with rising costs, it’s not always feasible.

We do, however, spend way too much money on cars.

People see cars as status symbols. Millions of people with office jobs and indoor hobbies overpay for giant pickup trucks they don’t need. Others buy fancy sports cars, luxury SUVs, and the fully loaded option of the once-affordable mid-size sedan.

With the average new car loan rate inching towards 7%, people are paying over $700 a month for their new cars.

That’s too much.

People also overspend on eating out and vices.

Better Things to Spend Money On

If you can reduce your car payment (I bought a brand-new car for less than $30K, and my payment is less than $400 a month) and limit eating out, you’ll have plenty of extra money to spend on the things that really matter.

So what are those things?

Spend Money on What You Love

The best things to spend money on (after necessities and saving!) are the things you love.

And that’s different for everyone.

Maybe you value that expensive, $750 per month pickup truck more than anything else in your life – you’re already doing it right.

But what if you don’t?

What if you’re dreaming of a different life, you can’t afford because most of your money is going to your stupid car and impulse buys on DoorDash?

It’s time to realign your spending with your priorities.

Here’s how.

Set Priorities

Spending money is about desire, so you must determine what you want.

Do you want a gorgeous house in the best neighborhood, or do you just want somewhere safe to live? Do you want a decked-out top-of-the-line Ford F150 pickup truck, or do you want a reliable car that gets you to and from work safely?

Because our salaries are limited, we likely can’t have everything we want. The next step is deciding what matters most.

What’s more important, the nice car or the big house? A secure retirement or a big pickup truck? All the things you want to do in life (travel, hang out with friends, take classes, etc.) or a nice house in the suburbs?

There is no wrong answer to any of these questions. Only you can decide what you value most in life.

However, you need to do it because it’s the only way to ensure you’re spending money on what matters most to you.

Examine Your Budget

Now that you know what you should spend money on, you need to see what you’re actually spending money on.

To do that, you need to take a long, hard look at your budget. Save receipts for a month. See where you’re spending money on stuff that doesn’t matter.

Armed with your actual expenditures, you can make changes to fix your spending.

Align Your Spending With Priorities

Now that you’ve set priorities and figured out where your money is going, it’s time to fix your budget to align your spending with the things you really want.

That may mean cutting back on things you thought you valued but realized aren’t necessary.

Trade in the nice car, downsize your home, and stop wasting money on things that don’t matter to you.

You may also find that you’re spending a lot of money on vices like alcohol, cigarettes, or fast food.

It’s time to cut that fat from your budget so you have extra money for your priorities.

Save and Invest

If you haven’t prioritized saving and investing yet, you need to. Life happens, but a fat nest egg will help you roll with the punches.

It may be boring, and you may ache to spend that juicy savings on something new and shiny, but it’s not worth it.

Think of saving as a bill. Pay it before spending any money on non-essentials.

But saving and investing are also crucial because it funds some of the things we value most, like:

- Housing

- Education (for our kids and us!)

- Retirement

- Travel & Adventure

If you prioritize any of these things, you need to either save or invest to make your dreams come true.

The Best Things to Spend Money On

Okay, I know I promised the best things to spend money on, and outside some throwaway lines, we haven’t delivered on that promise.

Part of that is because it’s different for everyone. I’m not you – I can’t decide what you value most. Only you can do that.

However, I can offer some ideas.

Here are my favorite things to spend money on.

Necessities

Okay, not my favorite, but crucial. I had a boyfriend once who blew all his money on video games and then couldn’t pay the rent.

Don’t be that guy.

Although you should absolutely try to save money on living expenses whenever possible, you still need to spend money on basic living. Everyone does.

Self-Improvement

Okay, now to my real favorites. Self-Improvement always tops my list of the best things to spend money on.

Take that class. Buy that book. Learn something new.

Self-actualization is key to happiness, and challenging yourself is one of the best ways to achieve it.

So spend money on things that make you a better person.

Hobbies

Hobbies keep us sane. They give us something interesting to do during our free time, but they also have tons of cool benefits, depending on the hobby.

Some get us outside into nature, others help us make friends. Creative hobbies keep our imaginations fresh, while crafting hobbies allow us to build something with our own two hands.

Engaging in green flag hobbies makes us better people – so spend your money on your favorite hobby and enjoy more of your free time.

Experiences

Life bursts with opportunity – are you making the most of it?

You can – if you spend money on new experiences. Try something new. Check crazy adventures off your bucket list.

It could be as simple as visiting a new town or trying a new restaurant, or as complex as sky diving or climbing a mountain.

The key is – doing something. In fact, when I was researching how to be happy, one of the experts I interviewed claimed that having new, fun experiences was the top path to happiness.

The data is clear – fresh new experiences are one of the best things to spend money on.

Travel

Travel is an experience, but I think it deserves its own section.

Travel teaches you things about the world, community, and yourself that you never would have anticipated. You get to meet new people, learn humanity’s history, engage with different cultures, widen your perspective, and see the world’s natural beauty.

I’ve traveled all over the world, and I’ll tell you each trip was worth every penny. Money well spent.

Pets

I don’t travel much anymore, but that’s mostly due to my favorite way to spend money: my cats.

They get the best prescription food money can buy, tons of treats and toys, a nice house, and their annual (expensive) vet care.

Yes, they cost an arm and a leg, but they bring me more joy than I ever imagined. I play with them and cuddle with them every day.

They’re one of the best parts of my life.

Helping Others

If you have more than enough money for yourself, why not spend any extra on helping others?

Donate money to charities that you believe in. Pay your friend’s tab at the bar. Set your children up for success by building generational wealth.

There’s nothing better than being able to treat people you love on occasion.

Anything that Enhances Your Life

I listed six of the best things to spend money on, but what if none of that speaks to you?

That’s okay.

Spend your money on whatever it is that enhances your life.

All I ask is that you set clear priorities and make sure that you’re spending money on the things you really want, rather than letting it slip away on things that don’t matter to you.

If you’re doing that, then you are spending money right.