Do you dream of living off a fat investment portfolio? Unless you’re already wealthy, you need compound interest.

When your interest compounds, your investments grow exponentially over time, as if by magic.

What is Compound Interest

What seems like magic is simply math.

Compound interest explains how the interest you earn adds up (or compounds) over time. It’s the financial term for making extra money from the interest you already earned.

It may seem negligible at first glance, but think of it like water. One tiny drop of water doesn’t do a thing, but millions of drops become mighty oceans.

How Does Compound Interest Work

Compound interest works by adding any interest gained to your principal for the next interest payment.

For example, let’s say you have $1000 invested, and you earn 10% interest per year, which compounds annually (Unrealistic, I know, but it makes it easy to visualize!).

After the first year, you’ll have $1100. But after the second year, you won’t have $1200, you’ll have $1210! That extra ten dollars came from the interest on the $100 you earned last year.

Over time, the money earned via compound interest can overtake your principal!

Time is Your Most Valuable Asset

We’ll show you all the math and how it works later, but the most crucial thing you need to know about compound interest is that time reigns supreme.

The sooner you start investing, the more time you have for compound interest to work its magic.

You must start investing as soon as possible – with your first paycheck from your first job. Make it work. If it’s too late for that, start today. Right now.

These examples will show you why.

Compound Interest Examples

Meet John and Sally, Pat. They’re all 50 years old, and each invested $100 per month for their investment timeframes, earning 5% interest that compounds daily.

John wanted to start working, fund his life, and build up his income before investing. He made his first investment at age 35.

Sally started investing with her first paycheck at age 22, but then life happened, and she wasn’t able to keep it up. She stopped investing at 35.

Pat started investing at 22 and never stopped.

Let’s see where they all are.

John has $27,017.

Sally has $46,914.

Pat has $73,720.

The chart below shows how each of their balances will grow over time.

| Age | Pat’s Balance | Pat’s Contributions | Sally’s Balance | Sally’s Contributions | John’s Balance | John’s Contributions |

| 22 | $100.00 | $100.00 | $100.00 | $100.00 | ||

| 23 | $1,335.55 | $1,300.00 | $1,335.55 | $1,300.00 | ||

| 24 | $2,634.44 | $2,500.00 | $2,634.44 | $2,500.00 | ||

| 25 | $3,999.92 | $3,700.00 | $3,999.92 | $3,700.00 | ||

| 26 | $5,435.40 | $4,900.00 | $5,435.40 | $4,900.00 | ||

| 27 | $6,944.48 | $6,100.00 | $6,944.48 | $6,100.00 | ||

| 28 | $8,530.93 | $7,300.00 | $8,530.93 | $7,300.00 | ||

| 29 | $10,198.71 | $8,500.00 | $10,198.71 | $8,500.00 | ||

| 30 | $11,951.99 | $9,700.00 | $11,951.99 | $9,700.00 | ||

| 31 | $13,795.16 | $10,900.00 | $13,795.16 | $10,900.00 | ||

| 32 | $15,732.82 | $12,100.00 | $15,732.82 | $12,100.00 | ||

| 33 | $17,769.82 | $13,300.00 | $17,769.82 | $13,300.00 | ||

| 34 | $19,911.26 | $14,500.00 | $19,911.26 | $14,500.00 | ||

| 35 | $22,162.48 | $15,700.00 | $22,162.48 | $15,700.00 | $100.00 | $100.00 |

| 36 | $24,529.11 | $16,900.00 | $22,162.48 | $22,162.48 | $1,335.55 | $1,300.00 |

| 37 | $27,017.08 | $18,100.00 | $23,298.69 | $22,162.48 | $2,634.44 | $2,500.00 |

| 38 | $29,632.60 | $19,300.00 | $24,493.16 | $22,162.48 | $3,999.92 | $3,700.00 |

| 39 | $32,382.21 | $20,500.00 | $25,748.86 | $22,162.48 | $5,435.40 | $4,900.00 |

| 40 | $35,272.78 | $21,700.00 | $27,068.94 | $22,162.48 | $6,944.48 | $6,100.00 |

| 41 | $38,311.55 | $22,900.00 | $28,456.70 | $22,162.48 | $8,530.93 | $7,300.00 |

| 42 | $41,506.11 | $24,100.00 | $29,915.60 | $22,162.48 | $10,198.71 | $8,500.00 |

| 43 | $44,864.44 | $25,300.00 | $31,449.30 | $22,162.48 | $11,951.99 | $9,700.00 |

| 44 | $48,394.95 | $26,500.00 | $33,061.63 | $22,162.48 | $13,795.16 | $10,900.00 |

| 45 | $52,106.45 | $27,700.00 | $34,756.62 | $22,162.48 | $15,732.82 | $12,100.00 |

| 46 | $56,008.24 | $28,900.00 | $36,538.50 | $22,162.48 | $17,769.82 | $13,300.00 |

| 47 | $60,110.06 | $30,100.00 | $38,411.74 | $22,162.48 | $19,911.26 | $14,500.00 |

| 48 | $64,422.18 | $31,300.00 | $40,381.01 | $22,162.48 | $22,162.48 | $15,700.00 |

| 49 | $68,955.36 | $32,500.00 | $42,451.25 | $22,162.48 | $24,529.11 | $16,900.00 |

| 50 | $73,720.95 | $33,700.00 | $44,627.61 | $22,162.48 | $27,017.08 | $18,100.00 |

Sally has nearly twice as much money as John, and she only invested a tiny bit more. She had more time for the magic of compound interest to work.

Of course, Pat is in the best position of all, because combined compound interest with additional principal for the entire time.

Compound Interest vs. Simple Interest

The alternative to compound interest is simple interest. If you have an investment earning simple interest, you don’t earn any additional money on your interest income; you only earn it on the principal.

So, in the example above, you would only have $1200 after the second year. You lost $10 because your investment doesn’t compound.

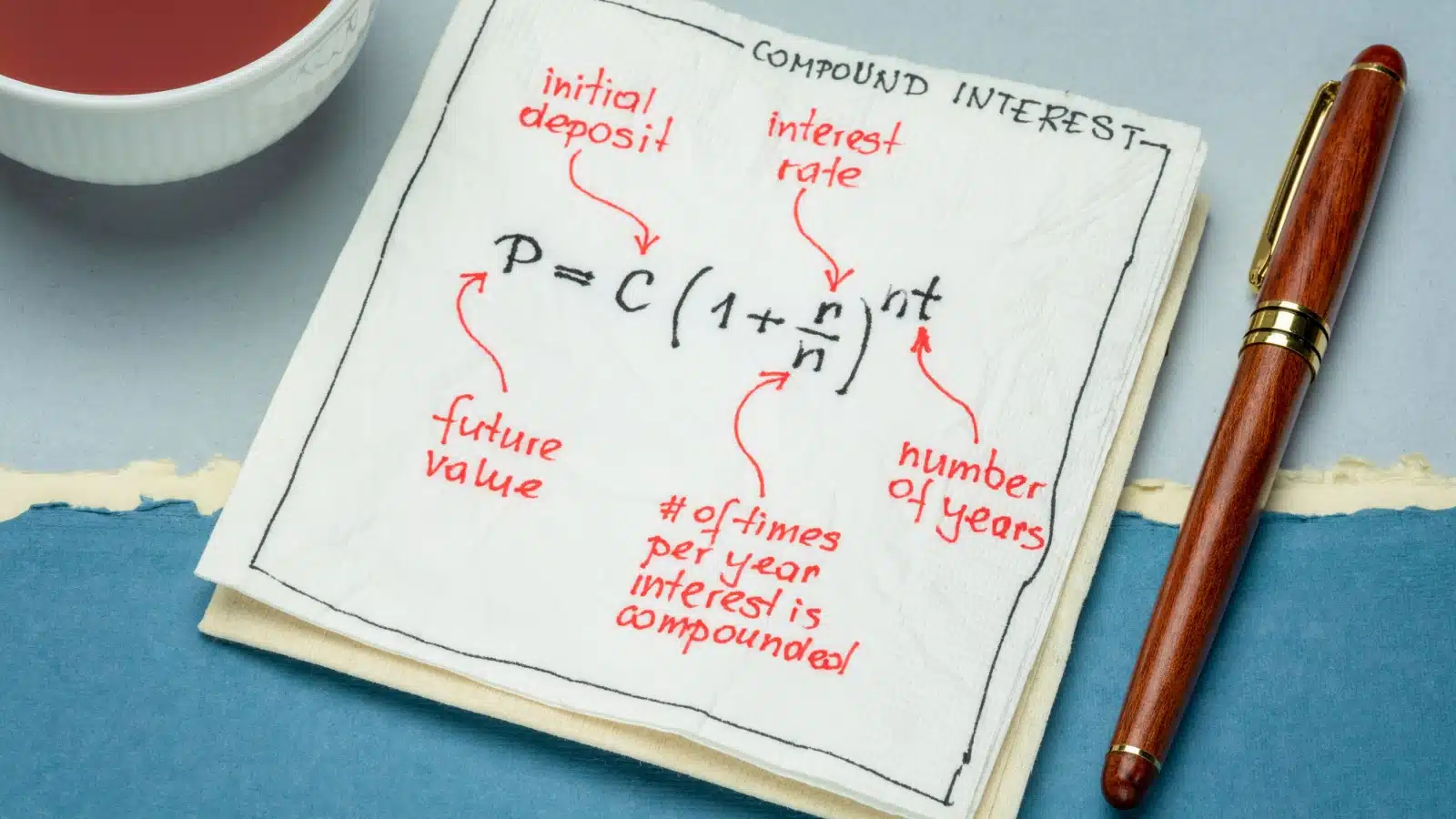

Formula for Compound Interest

You don’t need to know the formula for compound interest to make the magic work for you, but here it is in case you’re interested:

A = P(1 + r/n)nt

A – The amount you earn

P – Your principal (initial investment)

r – The interest rate

n – Number of times interest is compounded per year

t – Number of years

Using this formula, you can do basic calculations to see how much your money will grow over time.

Let’s use our $1000 at 10% interest compounded monthly to see how much it will grow in ten years:

A= 1000(1 + .1/12)12*10

A= 2707.04

If the interest didn’t compound, you’d only have $2000 after ten years. Compounding interest made you an extra $707, like magic!

Compound Interest Calculators

I get it, math is hard. But the good news is you don’t have to do it yourself.

The internet abounds with calculators, making it easy for you to see how much your investments will grow with the power of compound interest.

The U.S Securities and Exchange Commission offers an easy-to-use compound interest calculator at Investor.gov.

How to Make Compound Interest Work for You

fizkes via Shutterstock.com.

Anyone can use compound interest to grow wealth.

The most important thing you can do is start.

Put something, anything, into an account that earns compound interest.

These additional tips will help you make the most of it.

How Often it Compounds

There’s a massive difference between compounding daily and compounding annually.

Let’s go back to our first $1000.

Here’s the difference between whether it compounds daily, monthly, or yearly over ten years:

Daily: $2717

Monthly: $2707

Annually: $2593

To get the biggest bang for your buck, look for accounts that compound more often.

Interest Rate

When discussing compound interest, your rate matters – a lot! The higher the interest rate, the better, because you earn more money every time.

For example, look at the difference between $1000 invested in a 5% account that compounds annually, vs a 4% account that compounds daily over the course of ten years:

5% compounded annually = 1628

4% compounded daily = 1491

The account with the higher rate wins, even though it compounds less frequently.

Keep Investing

As you saw from the example, Pat’s nest egg is much larger than either John’s or Sally’s. That’s because he never stopped investing.

Compound interest is magical, and you can earn thousands of dollars without contributing another penny (like Sally did). But you will earn even more if you keep investing.

Savings vs Investing

I’ve used the word “investing” here in a broad sense that covers all types of accounts, but typically, interest is not paid on brokerage accounts or stocks. Usually, you only earn interest on things like savings accounts, certificates of deposit (CDs), or bonds.

But the same magic applies to traditional stock market investing through the power of dividends.

If you own a stock that pays dividends and reinvests your dividends, you’ll make a tiny bit more every time it pays. It’s not technically “compound interest” because you’re not earning interest, but the same general principles apply.

Start Now

The magic of compound investing works best with time, but it’s never too late.

The sooner you start, the sooner you will reap the benefits.